The insurance sector runs on vast volumes of documents and images. These massive data repositories power insurance activities such as underwriting, policy servicing, and claims processing, adjudication, and subrogation. Almost all communication associated with insurance claims involves documents and other data that is unstructured, including forms, emails, online chats, and more.

Extracting pertinent data from insurance documents has traditionally been a largely manual process performed by underwriters and insurance brokers. Workers may process insurance documents on their own or with some support from legacy technology like OCR.

Manual extraction of unstructured data is time consuming, costly and error-prone, and practically impossible for large insurance companies that insure millions of customers. While traditional OCRs help in digitizing data sources, and can perform rudimentary data extraction, they struggle to handle the variability that comes with complex documents (like those commonly used in the insurance industry). Low automation rates and inaccuracy make proprietary OCRs partial solutions that depend heavily on manual intervention and oversight by humans.

Modern Intelligent Document Processing (IDP) solutions can increase automation rates, and improve the accuracy of extracted data, unlocking new insurance workflow automations, lower costs, and improve claims turnaround times. This article explains the benefits of automating nine common insurance documents with IDP.

Intelligent Document Processing offers tangible results to many areas of the insurance sector. Below we cover the benefits of automatically processing some of the most common documents.

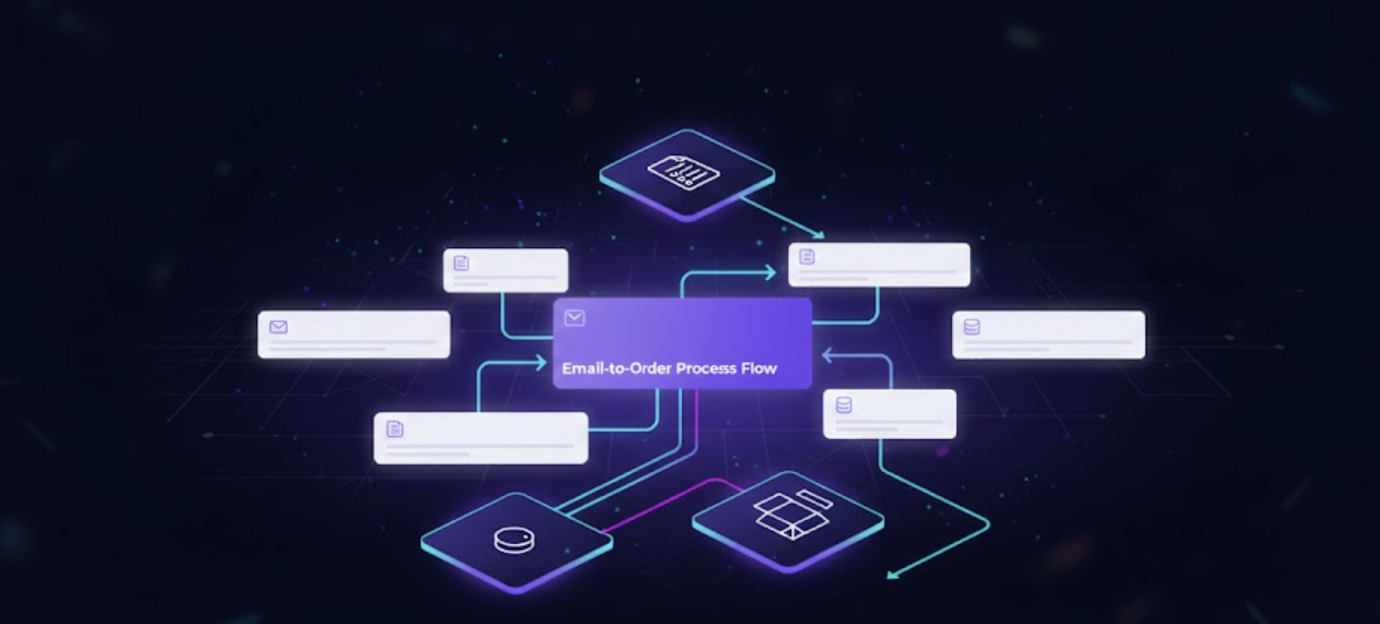

The first step in claim processing is claim incident reporting: The insurer or the beneficiary reports an event to the insurance company and submits all event-related documents with the claim request. Claims processing starts with obtaining all the information needed to decide on the claim’s validity and the appropriate action to be taken on it. Naturally, claim processing entails gathering vast amounts of data from numerous sources and collating them into a common platform in a meaningful way.

Claim incident reporting is the most tedious of the four tasks of claim processing. The manual extraction of relevant data from claim reports and all supporting documents takes several days. This is because insurance agents must collect data from a variety of sources including

Beyond time consumption, the manual extraction of relevant data from all claim-related data is fraught with risks of human errors such as mismatched financial data or customer details. Such details could result in loss to the customer, loss to the company, and scope for insurance fraud.

The use of IDP systems can reduce human intervention in insurance claim registration. IDP tools can process a range of documents and can automatically download, classify and compile user-defined data from different sources email attachments, transcripts, and scanned documents. Advanced IDP systems can also read, sort, analyze, and route emails.

IDPs can be combined with other automated workflow systems like RPA to automatically validate the extracted data against internal policy details, notify customers with claim numbers, and forward claim details to the investigative teams.

The FNOL is the first notice to be provided to an insurance agent/provider after an incident that would claim the benefits. It precedes the claim notification. For example in the case of auto insurance, a driver first informs the insurance company of the accident involving the vehicle. A claims adjuster is assigned who assesses the extent of damage and settlement amount. This may be based on

The details that the driver must provide to the adjuster include the policy number of their own vehicle and the other vehicle involved in the crash, date and time of the accident, location of the incident, police report number, and a personal account number.

The claim adjuster also uses unstructured descriptive data from other driver’s accounts and witnesses, and may even visit the accident scene to assess the degree. The adjuster may enter these data in a notebook, or in a digital format as raw data, that must be converted to structured form for further claim processing.

Insurance agencies often deal with the Deed of Trust that is sometimes used as an alternative to mortgage in a real estate transaction. It is a legally binding statement that the title of the property bought with a loan is held by a neutral third party (insurance company, escrow company, etc.) until the loan is paid off. Under a deed of trust, the legal title of the property belongs to the third party, the “trustee” until the loan is paid off. On loan default, the trustee becomes the owner of the property.

The Deed of Trust contains important information that is used for many insurance-based procedures such as certificate of title and title insurance. Title Insurance that protects lenders and homebuyers from financial loss sustained from defects in a title to a property, is granted by insurance companies and requires all information from the deed of trust. A certificate of title, on the other hand, is issued by a licensed attorney and provides the status of title, detailing all of the recorded documentation. It also acts as a guarantee for title insurance.

Despite their differences, title certification and insurance require filling of standard forms. In the US, these forms are designed and distributed by the American Land Title Association (ALTA). There are typically two forms,

All information requires data from the Deed of Trust and must be extracted accurately to avoid insurance fraud or errors. The title process is well suited for IDP in various steps:

The most commonly used Identification documents for Insurance purposes are Drivers' Licenses and Passports. The formats of driving licenses and passports vary with country, or even states within the same country. Photographs are almost always of poor resolution.

Traditional OCR solutions cannot handle the variations in format and inferior qualities of images. Furthermore, information in ID cards are extremely sensitive and privacy and security must be maintained at all times.

The use of ICP in processing IDs provides the following benefits:

Document-intensive policy operations include policy issuance, pre-underwriting checks, and updates. The management of an insurance policy involves managing data from various kinds of documents by the client, including

These documents are in various forms – as paper documents, pdfs, scanned images, faxed documents, etc., and therefore the data is extremely unstructured.

IDPs can extract inbound data from transcripts, emails, faxes, or other sources and include them in the company database properly structured, and/or required changes in the documents and internal systems.

IDPs can extract and manage the following information from policies and contracts, in addition to custom-fields that the insurance company may need to manage:

ML and NLP functionalities of IDPs can also help simplify and hasten other document-intensive operations associated with policy management, such as

Insurance companies, like any other enterprise, must deal with invoicing not only with respect to the insurance operation, but also for its internal operations such as commissions, salaries, incentives, and employee benefits of in-house employees.

Insurance Invoices are more complicated than regular invoices because insurance agencies are bound by state and federal laws that have stringent cancellation policies, which can have an effect on invoicing at every stage. For example, even when a policy is canceled because the premium has not been paid, the insurance company must show the default premium as revenue. This will be later written off as an expense. Thus, the invoice data that must be handled are complex in these cases.

Some insurance invoices are:

As can be understood from the above types of insurance invoices and the information they hold, the accounting personnel in insurance companies deal with a staggering amount of documents and data, most of which is unstructured. IDP can categorize the invoices into premium, credit intelligence, or collection invoice and populate appropriate fields from data extracted from other sources such as ID, credit records, transaction records, and tax information.

The insurance policy application form (sometimes called proposal) document must contain all vital information on the product or person being insured. Important aspects of the policy such as premiums, and the terms and conditions are based on the information provided in this document, and therefore must be accurate and verified. Some of the important details that must be recorded accurately include :

IDP, in synergy with RPA can be used to automate insurance policy application and issuance, thus reducing the amount of time and manual work required for this process.

Policy-holders also periodically submit various update requests, such as address change or update of bank mandates. Advanced IDP systems, especially when paired with RPA tools, can automatically identify change requests, classify supporting documents, and extract key data from all relevant documents. When paired with RPAs, this information, now in the form of structured data, can then be used to perform required updates and edits in the policy systems.

Title insurance protects lenders and homebuyers from financial loss sustained from defects in a title to a property. Title insurance may be lender’s or owner’s and are aimed to protect the lender and the buyer's equity in the property, respectively. It covers the following risks:

The title insurance certificate contains many legal jargons and property and ownership information that must be carefully entered into the database for insurance purposes. IDPs use Natural language Processing (NLP) and ML-based data extraction to pre-process insurance certificates and contracts so that all critical fields are extracted and categorized. Intelligent clause detection can enable other insurance management entities to easily access all pertinent information associated with the insurance cover.

Mortgage Underwriting is another area of insurance that is paperwork intensiveIt contains all information required for a mortgage loan, in addition to data such as debt-to-income ratio, income, and liability amounts.

Form1008 data is processed by loan underwriters process to help decide issuing a loan and the amount to be issued. This form is often received from different sources in varying formats such as hardcopy, email, or email attachments, and more recently through mobile applications. The variations in format and the inferiority of quality of scanned images makes it impossible to extract and manage data by legacy OCR systems. Manual processing is tedious and time-consuming, and sometimes impossible due to the volume of data that must be handled.

Some of the fields that must be accurately recorded are:

Underwriting operations can take days because of the variety of documents that must be processed. IDPs can extract underwriting documents from emails, classify and extract the required information, and cross-link and validate the application for completeness. They can be used in all of the five major steps of underwriting:

The rapid insurgence of AI and automation technology is expected to lead to disruptive changes in the insurance industry. To remain competitive, insurance companies are already adopting innovative approaches, harnessing cognitive learning insights from new data sources, and automating processes such as document management. IDPs can help insurance companies streamline document-heavy processes without compromising on accuracy or customer service. The use of IDP in the insurance sector can lead to the following benefits:

.svg)

%201.svg)